Six to twelve months after you buy an HVAC company, your insurance carrier will audit your payroll. If the previous owner used uninsured subcontractors or misclassified employees, you’re about to get a bill you didn’t budget for.

Nobody warns first-time HVAC buyers about the workers comp audit. It’s not in the broker’s listing. It’s not in the SBA checklist. It’s not something your attorney mentions at closing. And then, 9 months into your first year as an owner, an auditor from your insurance carrier shows up, asks for your payroll records, and hands you an additional premium bill that ranges from irritating to devastating.

Here’s what’s actually happening, why it catches new owners off guard, and how to prepare.

How Workers Comp Audits Work

Workers compensation insurance is priced on estimated payroll at the start of your policy. You tell the carrier how many employees you’ll have, what they do, and what you’ll pay them. The carrier multiplies that by the rate for your classification code — for HVAC work, that’s typically class code 5537 (Heating, Ventilation, AC Duct Work Installation) or 5183 (Plumbing), depending on the work mix.

At the end of the policy year, the carrier audits your actual payroll to see if the estimate was accurate. If you had more employees, paid higher wages, or used subcontractors who weren’t independently insured, the premium adjusts upward. You get a bill for the difference.

This happens every year. It’s routine. But for a new HVAC owner who just bought the company, the first audit covers your first full year of ownership — and that year is almost always messier than the estimate.

The Three Things That Blow Up Your First Audit

1. Uninsured Subcontractors

This is the big one. If the HVAC company you bought uses subcontractors — for install crews, duct fabrication, specialty refrigerant work, or overflow during busy season — and those subs do not carry their own workers compensation insurance, their payments get rolled into your payroll for premium calculation purposes.

Here’s the math. Say you paid $45,000 to a subcontractor crew over the summer for install overflow. They’re a two-person operation. They don’t carry workers comp (plenty of small sub crews don’t — it’s expensive and they’re trying to keep costs low).

Your insurance carrier will treat that $45,000 as if it were payroll you paid to your own employees, at class code 5537 rates. In most states, that’s $8–$15 per $100 of payroll. On $45,000:

- Low end: $45,000 × $8/$100 = $3,600 additional premium

- High end: $45,000 × $15/$100 = $6,750 additional premium

Now multiply that across every uninsured sub you used during the year.

The previous owner may have used the same subs for years without issue — because they never asked for certificates of insurance, and nobody checked. Your first audit is when the system catches up.

2. Payroll Misclassification

HVAC companies have two types of employees from a workers comp perspective:

- Field staff (technicians, installers, helpers) — classified under high-rate codes like 5537

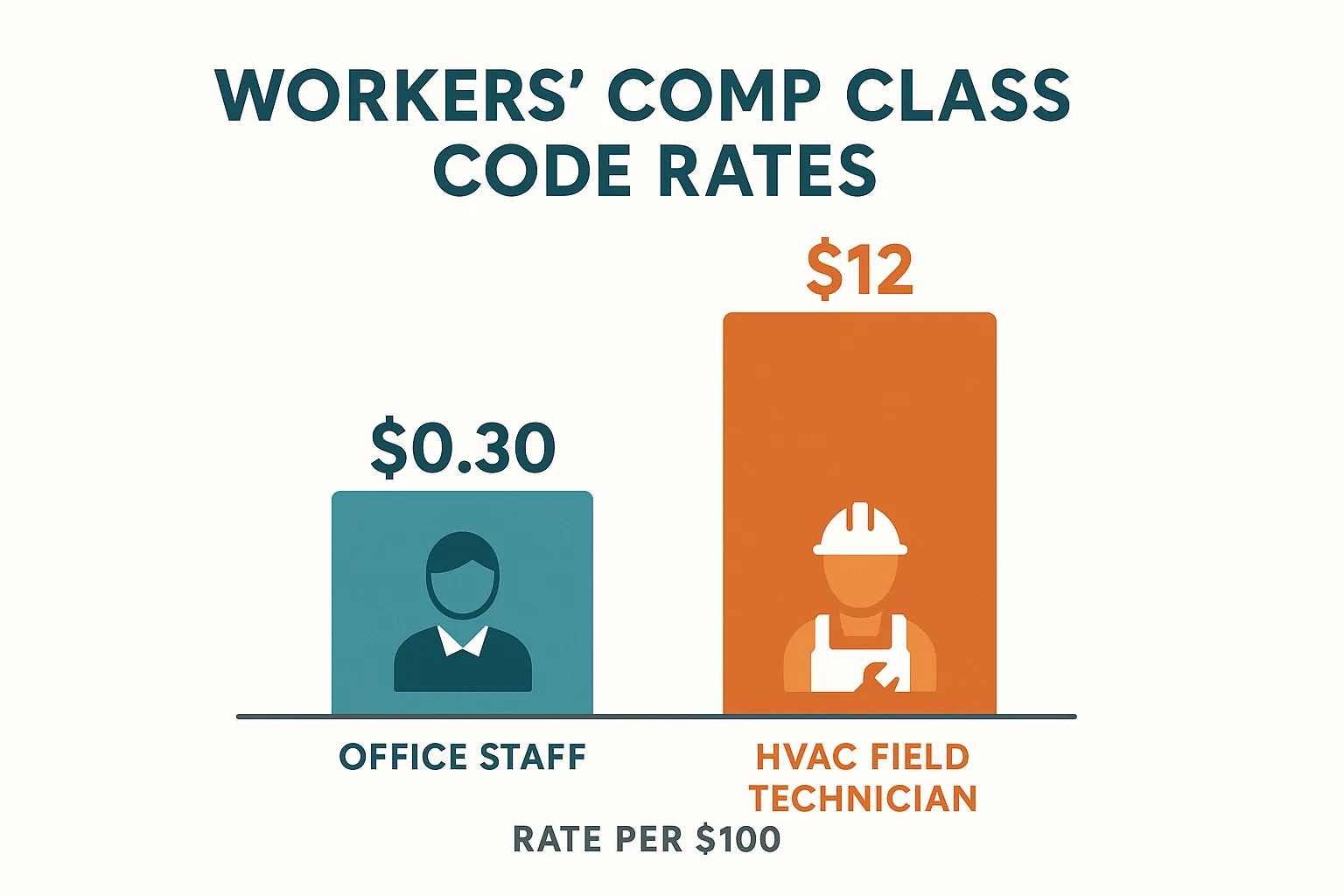

- Office staff (dispatchers, office managers, bookkeepers) — classified under low-rate codes like 8810 (Clerical)

The rate difference is massive. Field staff might cost $12 per $100 of payroll. Office staff might cost $0.30 per $100.

The problem: in many small HVAC shops, the line between office and field is blurry. The dispatcher who also runs parts on Saturdays. The office manager who occasionally rides along on commercial estimates. The owner’s spouse who does the books but also handles customer complaints on-site.

If the auditor determines that anyone classified as “office” actually performs field duties — even occasionally — their entire payroll gets reclassified at the field rate. One employee reclassified from 8810 to 5537 on $55,000 in annual wages:

- At 8810 rate: $55,000 × $0.30/$100 = $165/year

- At 5537 rate: $55,000 × $12/$100 = $6,600/year

- Audit adjustment: $6,435

3. Payroll Growth You Didn’t Report

If you hired during your first year — and most new HVAC owners do, especially heading into their first busy season — your actual payroll is higher than the estimate on your policy. That’s a straightforward adjustment, but it can be substantial.

Two additional technicians at $55K each = $110,000 in payroll you didn’t originally report. At $12/$100, that’s $13,200 in additional premium.

Combined with the sub and classification issues, it’s not unusual for a first-year HVAC owner to face an audit adjustment of $15,000–$30,000. On a company with $1M in revenue, that’s a meaningful hit to cash flow you didn’t plan for.

What You Should Have Done During Due Diligence

The workers comp mod rate gets checked during due diligence — and it should. But the mod rate tells you about the company’s claims history. It doesn’t tell you about classification accuracy or subcontractor insurance compliance. Those are separate issues.

Before closing, you or your insurance broker should have:

- Requested the previous owner’s most recent audit report. This shows how the carrier classified employees and whether there were prior adjustments. If the seller can’t produce it, that’s a yellow flag.

- Asked for certificates of insurance from every subcontractor. Not just “do you use subs?” but “show me the COIs.” If the seller can’t produce them, assume those subs are uninsured and price the risk accordingly.

- Reviewed job descriptions for every employee. Not titles — actual duties. Anyone who steps onto a job site, drives a company vehicle to a customer location, or handles equipment should be classified as field staff regardless of their title.

- Asked the seller’s insurance broker about prior audit adjustments. Were there any? How large? What triggered them? This is public information within the insurance relationship — the seller’s broker will tell you if asked.

What to Do Now (If You Already Own the Company)

If you’re past closing and heading toward your first audit, here’s your playbook:

Immediately:

- Collect certificates of insurance from every subcontractor. Today. If any sub can’t provide one, stop using them until they can — or factor their payments into your premium estimate.

- Review every employee’s classification with your insurance broker. Be honest about who goes into the field, even occasionally.

- Run your actual payroll numbers against the estimate on your policy. If you’re over, call your carrier and adjust mid-term. A voluntary mid-term adjustment costs the same but avoids the surprise.

Before the Audit:

- Organize your payroll records by classification code. The cleaner your records, the faster the audit, and the less room for the auditor to interpret ambiguously.

- Separate subcontractor payments from employee payroll in your accounting system. Have COIs ready to match against every sub payment.

- Know your experience modification rate and how claims during your first year affect it. A clean first year sets the trajectory for years of lower premiums.

Long-Term:

- Build subcontractor COI tracking into your standard operating procedure. No certificate, no work. No exceptions.

- Review classifications annually with your broker — job roles evolve, and what was accurate last year might not be this year.

- Budget for audit adjustments. Even with perfect records, minor adjustments are normal. Build a 5–10% premium buffer into your annual cost calendar.

The Number You Need to Know

For a typical 10–15 person HVAC company with $800K–$1.5M in revenue, workers compensation premiums run $25,000–$60,000 annually. A first-year audit adjustment of 20–40% is common for companies that change ownership. On a $40,000 premium, that’s $8,000–$16,000.

Budget for it. It’s not a disaster if you see it coming. It only becomes a crisis when it’s a surprise — and now it shouldn’t be.

Workers compensation rates and classification codes vary by state. The rates used in this article are representative national averages. Contact your state’s workers compensation board or a licensed insurance broker for rates specific to your location. NCCI class codes are standard in most states, but monopolistic states (Ohio, North Dakota, Washington, Wyoming) have their own systems.

Understanding insurance risk starts before closing. The insurance transfer gaps guide covers the broader insurance landscape during acquisitions, and The Hartford’s audit process explainer provides a carrier-side perspective on what auditors look for. For subcontractor coverage details, see Fisher Phillips’ analysis of contractor coverage impact.