You’re 45 days into due diligence. You’ve spent $15,000 on lawyers, accountants, and inspections. Then the seller calls: “We’ve received another offer.” Here’s how to respond without overpaying or walking away from a deal you’ve earned.

It’s happening more often than it used to. There are 2,400+ active investors on Axial alone seeking HVAC acquisitions in 2026. Private equity platforms are running aggressive outbound campaigns to HVAC owners. Search fund operators are sending personalized acquisition letters. And brokers are getting better at creating competitive tension — even when there’s only mild interest from a second party.

If you’re buying an HVAC company this year, the probability of encountering a competing offer during your due diligence is higher than it’s ever been. Capstone Partners reports 149 HVAC service transactions in the first half of 2026 alone — a 12.9% increase year-over-year. The question isn’t whether it will happen — it’s how you’ll respond when it does.

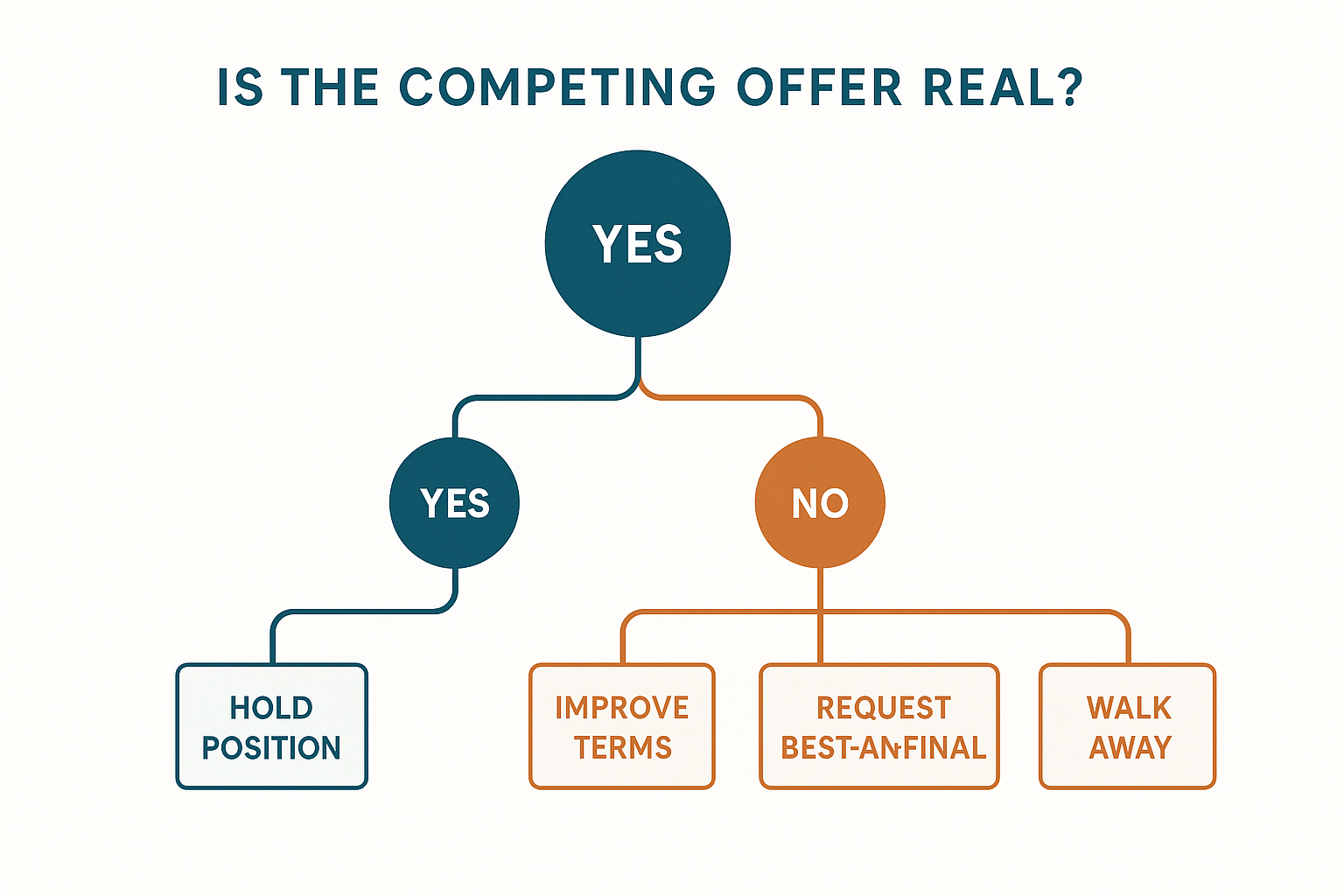

First: Is the Competing Offer Real?

This is the most important question and the hardest to answer. A significant percentage of “competing offers” are fabricated or exaggerated. Sellers — and especially their brokers — know that nothing accelerates a buyer’s timeline like the fear of losing the deal.

Signs the competing offer is legitimate:

- The seller or broker provides specific details: offer amount, structure, buyer type, timeline

- Your exclusivity period has expired (more on this below)

- The business was listed on multiple platforms or with a broker who actively markets to multiple buyers

- The seller seems genuinely conflicted, not strategically pressuring you

Signs it might be a pressure tactic:

- Vague language: “We’ve received interest” or “another party is looking at this” — interest is not an offer

- It arrives right when your due diligence is revealing problems — a convenient distraction from issues the seller doesn’t want you to focus on

- The seller says the other buyer will close faster but can’t explain how — most SBA loans take 60–90 days regardless of the buyer

- The broker won’t provide any details about the competing party, even basic information like buyer type (individual, PE, strategic)

- The timing coincides with a deadline you’ve set or a contingency you’ve flagged

You can’t always tell. But your response should be calibrated to your confidence level in the claim’s legitimacy.

The Cost of Walking Away

Before you decide how to respond, know what you’ve already invested. For a typical HVAC acquisition in the $800K–$2M range, your sunk costs at 45 days into due diligence include:

| Expense | Typical Range |

|---|---|

| Attorney fees (LOI review, asset purchase agreement draft) | $5,000–$12,000 |

| Accountant / quality of earnings review | $3,000–$8,000 |

| Environmental / facility inspection | $2,000–$6,000 |

| SBA application and appraisal fees | $2,000–$5,000 |

| Your time (dozens of hours away from your current job or business) | Substantial |

| Total sunk cost | $12,000–$31,000 |

Walking away from $20,000 in sunk costs is painful. But it’s not as painful as overpaying by $100,000 because you let competitive pressure override your valuation analysis.

The sunk cost fallacy is real. Your $20K is gone whether you close this deal or not. The decision framework is forward-looking: is this business worth the price at the terms you can get? As the International Business Brokers Association emphasizes in their deal process guidance, the competing offer changes the market dynamics, not the intrinsic value.

Your Five Options

Option 1: Hold Your Position

When to use it: When your current offer is fair, your due diligence is going well, and you believe the competing offer is either fabricated or weaker than yours.

How: Call the seller directly (not through the broker, if possible). Say something like: “I’ve heard there’s another interested party. My offer reflects what the business is worth based on my due diligence. I’m prepared to close on the timeline we agreed to. I’d rather not get into a bidding war — that doesn’t serve either of us.”

This works surprisingly often. Most sellers — especially retiring HVAC owners — value certainty over maximum price. A buyer who is 45 days into due diligence, has SBA pre-approval, and has demonstrated seriousness is worth more than a fresh LOI from an unknown buyer who hasn’t even toured the facility.

Option 2: Improve Terms, Not Price

When to use it: When you believe the competing offer is real and you need to strengthen your position without overpaying.

Ways to differentiate without raising your offer price:

- Accelerate your timeline. “I can close in 30 days instead of 60.” If your SBA lender can move faster (Preferred Lenders often can), this is a powerful differentiator. Preferred Lenders don’t need secondary SBA approval, shaving 2–4 weeks.

- Reduce contingencies. If your environmental inspection came back clean, waive that contingency. If the financial review looks solid, narrow the scope of remaining due diligence items. Every contingency you remove is one less reason for the deal to fall through.

- Increase the earnout or transition period. Offer a more generous seller transition consulting agreement — an additional 6 months at $5K/month gives the seller $30K more and costs you less than a $30K price increase because it’s spread over time and tied to actual transition support.

- Offer a larger down payment. If you have the cash, increasing your equity injection from 10% to 15% shows the seller (and the SBA) that you’re committed. It also reduces your loan amount, which can accelerate underwriting.

Option 3: Raise Your Price (Carefully)

When to use it: When you’ve confirmed the competing offer is real, it’s higher than yours, and the business is genuinely worth more than your current bid.

The key word is “genuinely.” Raising your price should be driven by your revised valuation analysis, not by competitive panic.

Before raising your price, answer these questions:

- What is the maximum this business is worth to you based on cash flow, not competitive pressure?

- At the higher price, does the debt service coverage ratio still work?

- Does the higher price change your return timeline?

- Would you still buy this business at the higher price if there were no competing offer?

If the answer to that last question is no, you’re bidding emotionally.

How much to raise: If you determine a price increase is justified, raise it by the minimum amount needed to be competitive — not the maximum you can afford. A 5–8% bump is typical. Going from $1.3M to $1.37M is reasonable if the financials support it. Going from $1.3M to $1.55M because “you really want this one” is how acquirers default on their SBA loans.

Option 4: Request a Best-and-Final Process

When to use it: When the seller or broker is creating an auction dynamic, and you’d rather compete transparently than through back-channel pressure.

Tell the broker: “If you’re running a competitive process, let’s formalize it. Set a deadline for best-and-final offers. I’ll submit mine, the other party submits theirs, and you choose. But I’m not going to negotiate against a ghost — I need to know this is a real process.”

This forces transparency. If the competing offer is real, the broker will agree — it benefits them to have a structured process. If it’s fabricated, the broker will usually back down and your original terms hold.

Option 5: Walk Away

When to use it: When the price needed to win the deal exceeds the value you’ve established through due diligence, or when the competitive dynamics suggest the deal will be painful regardless of outcome.

Walking away is always an option and sometimes the best one. Specific triggers:

- The competing buyer is a PE platform that can pay strategic multiples you can’t match — they’re buying market share, not cash flow

- The seller is using the competing offer to renegotiate deal terms you already agreed to — not just price, but holdback, escrow, or indemnification provisions

- The process feels manipulative — multiple rounds of “just one more bid” that never seem to end

- You’ve discovered issues during due diligence that the competitive pressure is causing you to minimize

Protecting Yourself Before It Happens

The best defense against competing offers is structural: build exclusivity into your LOI from the start.

Exclusivity provisions that work:

- 60–90 day exclusivity period from LOI signing through close — the seller agrees not to market the business or entertain other offers during this window. The SBA Standard Operating Procedure expects lenders to confirm exclusivity before committing to underwriting, so this isn’t just a negotiation preference — it’s a lending requirement

- Breakup fee if the seller accepts another offer during the exclusivity period — typically 1–2% of the purchase price ($12,000–$30,000 on a $1.5M deal). This doesn’t prevent the seller from accepting a better offer, but it compensates you for sunk costs.

- No-shop clause that requires the seller to notify you of any unsolicited offers and give you the right to match — a “right of first refusal” within the exclusivity window

Most brokers resist strong exclusivity clauses because they reduce the broker’s leverage. Push for them anyway. An LOI without exclusivity is a non-binding statement of interest, not a deal in progress.

The Emotional Discipline

The hardest part of handling a competing offer isn’t the negotiation — it’s managing your own psychology.

You’ve spent weeks learning this business. You’ve imagined yourself running it. You’ve told your spouse about it. You’ve started mentally redesigning the shop. You may have already picked out which trucks to replace.

When someone threatens to take that away, every instinct says: fight. Outbid. Win.

That instinct is why overpayment happens. Research from Harvard Business Review on acquisition psychology confirms that competitive bidding consistently drives acquirers past rational price ceilings. The deal you lose is the one you don’t close. The deal that ruins you is the one you overpay to win.

Set your walk-away number before you enter due diligence. Write it down. Show it to your CPA and attorney. When a competing offer arrives, pull out that number. If winning requires exceeding it, walk — and trust that another HVAC company will come to market within 6 months, because with the retirement wave in full swing, it will.

The best acquisitions are built on discipline, not desperation.

For a step-by-step walkthrough of LOI structure, exclusivity provisions, and the full due diligence process, see the HVAC Acquisition Chapter Guide. If you’re currently facing a competing offer and need to evaluate your options quickly, start with the valuation math to confirm your ceiling before responding.