You survived your first acquisition. You built it into something real. Now you’re eyeing a second shop — and every piece of advice you find is written for PE platforms with integration teams, centralized dispatch, and a CFO on payroll. This one isn’t.

You know what nobody tells you about going from one location to two?

It’s harder than going from zero to one. Not because the deal mechanics are more complex — though deal #2 does work differently. It’s harder because when you bought your first shop, you had time to focus on it. You could spend every day in the building, learning the team, learning the customers, learning where the bodies were buried.

With a second shop, that’s not the whole job anymore. That’s half the job. The other half is making sure your first shop doesn’t fall apart while you’re gone.

Private equity firms that do five add-ons a year have entire departments for this. Regional operations managers, integration playbooks, centralized accounting, shared dispatch. You have yourself, probably one office manager, and a solid lead tech who you’re quietly terrified might leave.

This is the playbook written for that reality. When you’re actually ready, how deal #2 is structurally different, what to look for in the right target, and how to manage two shops without the infrastructure PE takes for granted.

Are You Actually Ready? (The Signals That Don’t Lie)

The instinct to grow hits most HVAC owners somewhere around year two of running their first acquisition. Revenue is trending up, the loan is getting paid down, and you’re watching PE roll into your market and buying everything in sight.

Slow down.

Most independent owners who struggle with their second acquisition weren’t bad at acquisitions. They were just too early.

Financial signals that say you’re ready

Your first shop is truly stable, not just profitable. There’s a difference. Profitable means the numbers work. Stable means it would keep working if you weren’t there for a month. If your revenue is tied to your personal customer relationships, your daily presence in dispatch, or your van on the road — the business is not stable, it’s dependent. Fix that first.

You have 3–6 months of operating cash in reserve. Two shops means two payrolls, two insurance bills, two sets of vehicle payments. You will have months where both shops hit a slow stretch simultaneously. If your cushion is thin, a bad February at shop #1 plus a rough integration at shop #2 is not a math problem — it’s a survival problem.

Your debt service coverage ratio (DSCR) leaves room. You’re probably carrying SBA debt from acquisition #1. Lenders want to see that your existing business generates enough cash flow to support its current obligations AND the new acquisition. The rule of thumb is 1.25x DSCR on the combined picture. If you’re at 1.3x DSCR on business #1 alone, you have room. If you’re at 1.1x, you probably don’t qualify for another SBA loan until that ratio improves.

Your first acquisition is at least 18 months post-close. This isn’t a hard rule. But most of the operational fires from acquisition #1 — staff turnover, customer attrition, system migrations, the equipment surprises the seller “forgot” to mention — settle out in that window. Buying #2 while still fighting fires at #1 is how people end up with two problem businesses instead of one.

Operational signals that say you’re ready

You have a service manager who runs day-to-day without you. If you need to be in the building to prevent chaos, you don’t have a business — you have a job. Before you look at a second acquisition, make sure shop #1 has someone capable of running the floor, handling dispatch, managing tech scheduling, and dealing with callbacks when you’re not around.

Your technicians aren’t leaving. High turnover at shop #1 is a flashing warning light. You cannot absorb the distraction of a second integration when you’re constantly replacing techs at your existing location. The best technicians from a shop you acquire will test you immediately — they’ll look for instability, for chaos, for a reason to leave. If your existing operation has that instability, you will lose people at both shops.

Your processes are documented. You don’t need a 400-page operations manual. But you do need written SOPs for job costing, dispatch protocol, service call closure, and maintenance agreement scheduling. If every process lives in your head, you can’t replicate it at a second location. And if you can’t replicate it, what exactly are you scaling?

How Deal #2 Works Differently Than Deal #1

When you bought your first HVAC company, you were starting from zero. No track record, no existing customer base, probably a nervous banker running credit checks on everything you owned.

Deal #2 is different. You have leverage now.

You have a proof of concept

Lenders love repeat buyers. A second SBA acquisition from a buyer who has successfully operated their first acquisition for 18+ months is a materially lower risk profile than a first-time buyer. You’ve demonstrated you can run an HVAC business, manage debt service, and keep the lights on through a slow season.

Use this. When you talk to lenders, lead with your track record — specifically the DSCR on your first acquisition and the revenue/SDE growth since you took over.

Your existing business is an asset in the deal

When you acquired shop #1, you were offering the seller a purchase price and some personality. For shop #2, you’re offering something more concrete:

- An established customer base that can absorb their overflow

- An existing maintenance agreement machine that their customers can roll into

- Shared overhead that makes both businesses more profitable post-integration

- A local reputation and operating history

This matters most when you’re competing against someone who’s never run a shop. A seller who cares about their business landing with someone competent will weight your track record.

The structure should be different

Your first deal was probably straightforward — asset purchase, SBA 7(a) financing, maybe a small seller note. Deal #2 gives you more structural flexibility.

Seller financing percentage: On a first deal, asking for 25% seller financing is unusual. On a second deal from a buyer with an existing operation and demonstrated track record, sellers are more comfortable carrying paper. A larger seller note (15–25% of the purchase price) reduces your SBA loan balance and your monthly debt service. It also gives the seller ongoing income and keeps them financially motivated to support a smooth transition.

Earnout structures: These are rare in small HVAC deals but occasionally worth considering when the seller’s asking price is based on revenue projections that feel optimistic. An earnout ties a portion of the purchase price to post-close performance — seller gets paid if the business hits the numbers they claimed. Use these surgically. The administrative and relationship cost of tracking earnouts is real, and they create friction with the seller during transition.

Asset vs. stock: Always lean toward asset purchase unless there’s a specific reason to buy stock (like an operating license that doesn’t transfer in an asset deal — check the licensing rules in your state carefully). Asset purchases let you leave liabilities behind and reset the equipment depreciation schedule. Same as deal #1, but worth repeating.

The transition period: This is where deal #2 should look meaningfully different from your first acquisition. You know now — because you’ve been through it — how much knowledge lives in the seller’s head. Negotiate a longer transition period: 6–12 months of the seller available as a consultant, with a clear schedule and modest monthly compensation ($3,000–6,000/month is typical). The introductions they make, the customer relationships they hand off, the institutional knowledge they carry — that’s worth every dollar.

What to Look for in Target #2

Not every HVAC company is a good fit for a single-owner two-location operation. PE platforms can integrate any shape of business because they have the infrastructure to reshape it. You don’t. Target #2 needs to be additive, not complicated.

Geography first

The ideal second shop is 20–60 miles from your first location. Close enough to share some resources — specific vendors, overflow dispatch, equipment loaners, the occasional tech who can cover both markets in a pinch. Far enough that you’re not cannibalizing your own customers.

The same-city second location sounds appealing but often creates pricing confusion, brand overlap, and internal competition for jobs. Different enough market to feel separate. Close enough to feel connected.

Contiguous service area is the gold standard. If shop #1 covers the north suburbs and shop #2 covers the adjacent county, you’ve now got a continuous territory. You can market to the edge of both zones with one campaign. You can send a tech from either shop without a dead-hour drive.

Revenue mix compatibility

Look for a second shop with a similar service mix to your first — or one that fills a gap you’re deliberately targeting.

If your first shop is 70% residential service and you want to grow commercial, a second acquisition that’s 50% light commercial is an accelerant. You’ve got the residential operations down; the second location teaches you commercial at a smaller scale before you bet the whole operation on it.

What to avoid: a second shop that’s radically different from your first. If your first acquisition is pure residential and the second one is 80% mechanical contracting with a few large commercial contracts, you’re not scaling — you’re learning a different business. That’s not a bad deal, it’s just a first deal, and you should evaluate it that way.

Maintenance agreement base

This matters even more in deal #2 than deal #1.

Here’s why: when you integrate two shops, the biggest operational win is migrating both agreement bases onto the same scheduling system and routing the visits efficiently. A second shop with 800 active maintenance agreements creates 1,600 service visits per year that you can route alongside your existing agreement base. The overhead to run those 800 extra visits is much lower when you already have the infrastructure in place.

A second shop with zero maintenance agreements? You’re starting that build from scratch while also integrating the business. Possible, but it’s work you’ll feel.

Minimum threshold: the target should have at least 300–400 active agreements. Anything less and the recurring revenue story is more hope than reality.

Cultural fit (and I mean this tactically, not sentimentally)

The owner’s relationship with their technicians is either going to make your integration or blow it up.

If the seller runs a shop where techs have been there for 8 years and loyalty is personal — loyalty to the owner — you need the seller to make a genuine handoff. You need them in the shop, introducing you, explaining why this is good news, vouching for you. That transition won’t happen if the seller is resentful about the sale or checked out before it closes.

If the seller has high turnover, a toxic dispatch culture, or a shop where three techs run everything and the rest are temps — that’s a different problem. You can fix it, but it’s expensive in time and sometimes in payroll, because you’ll lose people before you can stabilize.

Talk to the front-line techs during due diligence. Not formally, not in a conference room. Find a reason to walk the shop floor, ask about the job board, ask what they like about working there. What you hear will tell you more than any financial statement.

The Operational Reality of Two Shops

Here’s the part that catches people off guard: the work of running two shops isn’t twice the work of running one. It’s different work.

Dispatch and scheduling

Single-location dispatch is relatively simple. You know your territory, your tech availability, your drive times. Everything is local.

Two locations means two service areas, two sets of tech schedules, and a question that comes up every day: do you centralize dispatch or run it separately?

For most independent operators starting their second location: keep dispatch separate for the first 12 months. The second shop has its own territory, its own routing patterns, and its own customer relationships. Running dispatch from your first shop’s office adds cognitive load and creates service errors — the dispatcher sends a tech from shop #1 on a job that’s 45 minutes closer to shop #2 because they forgot to check the schedule.

After the first year, when you understand both territories and have built the team, consolidated dispatch starts making sense. The efficiency gains are real: better route density, fewer empty-miles drives, the ability to flex capacity across locations when one market is slow and the other is running hot. But earn it. Don’t mandate it on day 60 because it sounds efficient.

Inventory and parts

Your second shop needs its own core parts inventory. Same categories as the first — common capacitors, contactors, basic controls, filters. Don’t assume you can run a van to shop #1 when a tech at shop #2 needs a part.

Where you do get leverage: bulk purchasing. Two shops buying together can hit pricing thresholds your first location couldn’t touch alone. Negotiate supplier pricing based on combined volume across both shops. This takes about three months to set up properly, but the pricing difference is material — 10–15% on frequently used parts adds up over a year.

Fleet and equipment

The second shop’s fleet is the second shop’s fleet. Don’t cross the streams.

This sounds obvious until you’re three months in and a tech at shop #2 has a box truck in the shop for repair and you’re considering lending them a van from shop #1 “just for a week.” Don’t. Once equipment starts moving between locations without a formal process, your fleet tracking breaks down, your insurance certificates get complicated, and your ops manager spends six hours a week playing “where’s the van.”

If the fleet needs supplementing, buy or lease the right equipment for the location. Keep the books clean.

Finance and accounting

Two shops, two sets of books — at least internally. You need to know which location is profitable and which isn’t. If you consolidate everything into one P&L from day one, you lose the visibility to know whether shop #2 is performing to expectations or quietly bleeding.

Set up shop-level P&L tracking from day one. Same chart of accounts, same categories, separate location codes. Your bookkeeper or accountant should be able to pull a monthly P&L for each location with five minutes of work. If that’s not possible, fix it before you close on the second deal.

The Integration Timeline: What 6–12 Months Actually Looks Like

Integration timelines in PE playbooks assume resources you don’t have. Here’s a realistic month-by-month plan for an independent operator.

Months 1–2: Don’t touch much

Your primary job in the first 60 days is to not break what works.

Show up. Learn the team. Understand the existing dispatch process, the dispatch problems, the customer complaints that recur, the techs who are indispensable and the ones who were borderline. Meet the top 20 commercial customers in person. Get into the service records.

Do not: change the software yet, change the pricing structure yet, merge the dispatch yet, change the company name yet (unless there’s a specific and compelling reason). Every change you make in the first 60 days is a change before you fully understand what you’re changing.

The one exception: if you see something immediately illegal, unsafe, or actively harmful — environmental compliance issues, unlicensed tech running refrigerant, payroll fraud — address it immediately. Everything else can wait.

Months 3–4: Standardize the back end

This is when you migrate to a common operating platform (ServiceTitan, Housecall Pro, whatever you run at shop #1) if the second shop is on a different system.

This is also when you set up the joint accounting structure, bring the second shop’s bookkeeping onto your existing accountant’s workflow, and standardize job costing categories so your financials are comparable across both locations.

Start cross-selling maintenance agreements from shop #1’s customer list in shop #2’s territory. If you have residential customers near the boundary of your territories, this is when you start migrating some of that work to the closer shop.

Months 5–8: Cross-selling and cross-training

By now, both shops should be running relatively independently. This is when you start extracting the synergies.

Route joint maintenance agreement visits for efficiency. If you have agreement customers in the overlap zone between the two shops, assign visits based on tech availability rather than shop boundary.

Cross-train your leads. Your best lead tech from shop #1 should visit shop #2 for a week — and vice versa. They’ll share technical approaches, workflow habits, and product preferences. This isn’t just training; it’s culture transfer. The tech community across both shops starts to feel like one company.

Start evaluating whether consolidated dispatch makes sense. It probably does by month 6–8 if both locations are stable.

Months 9–12: Evaluate the math

By the end of year one, you should have enough data to compare:

- Actual vs. projected revenue at shop #2

- Actual vs. projected SDE at shop #2

- Combined overhead as a percentage of combined revenue (it should be lower than each shop independently)

- Tech retention at both locations

If the second shop is performing to projection and overhead is actually compressing as a percentage, you’re doing it right. If you’re still running two separate dispatch systems, two separate inventory processes, and two sets of books that never talk to each other — you haven’t integrated, you’ve just acquired. Those are different things.

The Math: When Two Shops Are More Profitable Than Double One

This is the part that actually justifies the second acquisition.

When PE firms buy add-on companies, the financial thesis is straightforward: shared overhead means the combined entity is more profitable per dollar of revenue than either company independently. Two shops should not cost twice as much to run as one shop.

Here’s what that looks like in practice.

Fixed overhead that doesn’t double:

- Owner’s salary and benefits: you’re one person running two shops, not two people. That’s roughly $80,000–120,000 in annual overhead that doesn’t replicate.

- Insurance (E&O, GL, fleet policy): a multi-location policy does not cost twice a single-location policy. Expect 50–70% of the second shop’s standalone insurance cost.

- Software subscriptions: ServiceTitan or equivalent at the enterprise tier covers multiple locations. You’re not paying a second full license.

- Bookkeeping and accounting: one accountant handles two sets of books at a rate lower than two separate accountants.

- Marketing infrastructure: your website, your Google Ads, your review strategy — these scale across markets without doubling.

What the math actually looks like:

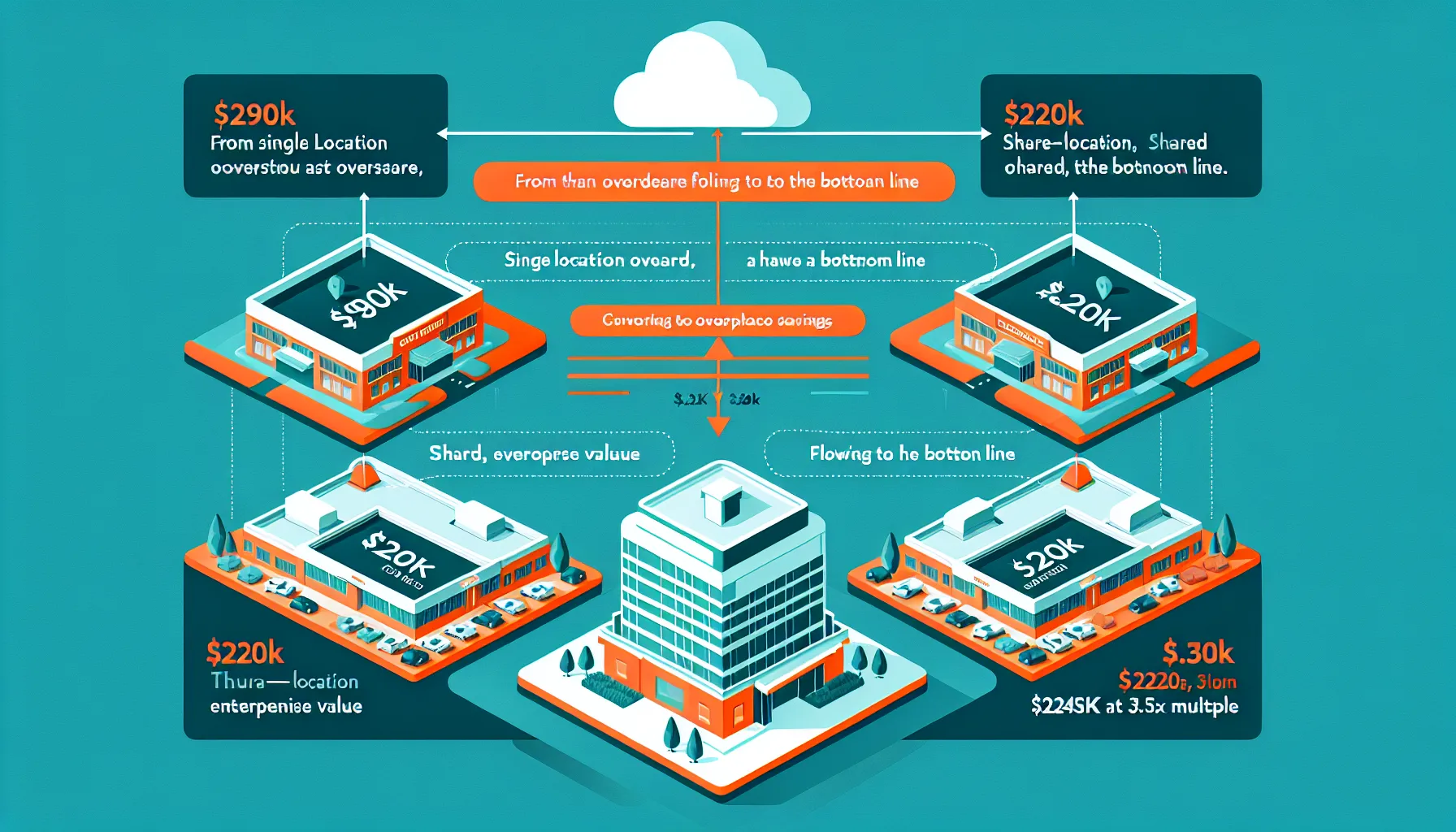

Let’s say shop #1 does $1.5M in revenue with $350K in SDE. Fixed overhead (you personally, insurance, software, accounting, marketing) is roughly $160K of that.

You acquire shop #2 at $1.2M revenue and $280K in SDE. Standalone, that business has its own full overhead of $130K.

Combined overhead is not $160K + $130K = $290K. It’s more like $220K — because your salary doesn’t double, your software doesn’t double, your accounting doesn’t double.

That $70K in shared overhead savings goes straight to the bottom line of the combined operation. At a 3.5x EBITDA multiple, that overhead compression is worth $245K in enterprise value. On top of that, the cross-selling of maintenance agreements, the routing efficiency, and the purchasing leverage may generate another $30–60K in annual cash flow.

The combined business is worth more than the sum of its parts. That’s the point.

Common Mistakes Independent Owners Make on Their Second Deal

These are the patterns I’ve watched play out. None of them are fatal. All of them are avoidable.

Moving too fast because the first deal felt easy

The first deal was hard. You just forgot. When something goes well, memory smooths the rough edges. The second deal will have its own surprises. Budget for them — in time and in cash.

Underestimating the seller transition

You know the deal terms. You understand the assets you’re buying. But the institutional knowledge that lives in the seller’s head — the commercial account relationship, the quirky residential customer who calls four times before scheduling, the tech who quit twice before deciding to stay — that’s not in any document.

Most buyers spend 80% of their transition energy on the paperwork and 20% on the relationship transfer. It should be the inverse. Get the seller out of their truck and into your new customers’ conference rooms.

Letting shop #1 drift

This is the most common and most expensive mistake.

When you’re excited about the second deal, your attention shifts. The service manager at shop #1 starts making calls they should be escalating. The agreement renewal rate slips two points because nobody’s following up. A tech leaves and the replacement hire is rushed.

You don’t notice any of this until three months later when shop #1’s SDE is down 12% and you can’t figure out why.

Set up a weekly ops call with your shop #1 service manager. Review the same five metrics every week: revenue, call volume, agreement count, tech utilization, callbacks. Takes 30 minutes. Keeps you in the loop without requiring your physical presence.

Overpaying because the deal feels strategic

Deal #2 feels different than deal #1. You’re not just buying a business — you’re building a company. That narrative can make a mediocre deal feel strategic. It isn’t.

The math still has to work. The debt service coverage still has to work. The seller’s claims about revenue still need to be verified. The fleet still needs a physical inspection.

The strategic value of a second location is real. But it gets realized over years of operations, not at the closing table. Price the deal on the fundamentals and let the strategy pay off over time.

Not telling your existing team what’s happening

Your techs at shop #1 will find out about the acquisition — either from you, or from a customer who saw it in the local paper, or from the rumor mill. Which version do you want them to hear?

Telling your team directly, early, and honestly costs you a one-hour team meeting. It buys you loyalty through a disruptive period. It also gives you a chance to recruit the best techs to take on additional responsibilities at shop #2 — the ambitious lead tech who’s been asking for more might just become your shop #2 field supervisor.

Frequently Asked Questions

How long should I own my first HVAC company before buying a second?

The minimum viable timeline is 18 months post-close, but the better question is whether your first shop has a stable service manager, consistent cash flow, and documented processes. Most operators hit that point somewhere between 18 and 36 months after their first acquisition.

Can I use SBA financing to buy my second HVAC company?

Yes, with conditions. The SBA limits total exposure per borrower (currently $5M for 7(a) loans), and your lender will evaluate the combined debt service picture — both your existing SBA loan and the new one. The key number is combined DSCR across both businesses. Get pre-qualified before you start shopping; it’s a different calculation than your first deal.

How far apart should my two HVAC locations be?

For most independent operators, 20–60 miles is the sweet spot. Close enough to share resources and routing efficiency, far enough that you’re not cannibalizing your own territory. Contiguous service areas are ideal.

Should I keep the second company’s name or rebrand it?

Keeping the name for at least 12–18 months post-acquisition is almost always the right move. The second shop’s customer relationships are tied to that brand. Changing it too fast creates confusion and can accelerate customer attrition. You can integrate the brand gradually — same look, same colors, eventually same name — but do it over time. See the marketing playbook for the rebrand decision framework.

How do I handle tech turnover during integration?

Expect some. A new owner is a change event, and change makes people nervous. The best defense is transparency and speed: communicate early, communicate honestly, and identify the 2–3 technicians who are informal leaders in the shop. Win them over first. If those people are supportive of the transition, the rest of the team takes its cues accordingly. Read the full employee retention playbook.

What DSCR do I need to qualify for a second SBA acquisition loan?

SBA lenders typically want to see 1.25x DSCR on a combined basis — meaning the cash flow from both businesses, after paying all existing debt service, still covers the new acquisition’s debt payments by 1.25x. Some lenders want 1.35–1.50x for a second acquisition. Run your existing DSCR first; that number tells you how much headroom you have for additional debt. Compare your options with the variable rate risk guide.

The Bottom Line

PE firms make the one-to-two transition look systematic because they have the infrastructure to make it systematic. You’re building that infrastructure from scratch, one deal at a time.

That’s not a disadvantage. It’s actually an edge — because the businesses PE is buying at 5–6x SDE are not the same businesses you should be buying at 3–3.5x. You’re in a different market, building a different kind of company.

One shop done right is a job that pays well. Two shops done right is a business that builds wealth.

But the sequence matters. Get shop #1 stable, profitable, and operationally independent of your daily presence. Build the cash reserve. Find the right geographic target. Structure deal #2 with more seller financing and a longer transition than your first deal.

Then do it once. Not three times in 18 months like you’re running a fund.

Build the second location into a real business before you start looking at a third. The operators who scale sustainably go deep before they go wide. Two shops running at 92% of potential are worth more — and are less likely to blow up — than three shops running at 60%.

The math works. The operations can work. Give yourself the time to make them.